GREAT BAY--Members of Parliament used the General Audit Chamber’s appearance in a Central Committee meeting on Tuesday, February 10, 2026, to press for clearer follow-up on audit recommendations and greater public accountability in government processes. Two of the sharpest lines of questioning came from Members of Parliament Ardwell Irion and Egbert Doran.

Irion cautioned the Chamber about the tone and content of its annual reporting, arguing it risks reading as self-praise if it highlights achievements without demonstrating impact and follow-up, while Doran sought a definitive answer on whether the process related to public support for the Soul Beach Music Festival will be audited.

MP Doran built his questions around a paper trail, and around a single premise: once the legislature has adopted a motion requesting an audit into the public side of a major event, the oversight body should not be steering Parliament toward alternative tools, or advising it to outsource the work.

By the end of the session, the Chamber signaled that the Soul Beach process will be audited as part of its 2026 work, a clarification that MP Doran later welcomed as the missing “yes or no” that had fueled months of friction.

Doran: Parliament’s request on Soul Beach

MP Doran’s questions centered on Parliament’s previously adopted motion requesting a review of the financial and administrative process related to public support for the Soul Beach Music Festival. He referenced the motion adopted on June 23, 2025, which requested an independent review of the application and approval process, legal advice obtained, budgetary allocations, payment mechanisms, the relevant decision-making, public financial and in-kind contributions, documentation, and adherence to applicable legal procedures.

Doran emphasized that the request should be understood as a decision of Parliament as a body, not as an informal inquiry by an individual MP. He also stressed that the intent was to examine the public process and the use of public resources, not to audit private sponsors or private contributions.

He questioned why the Audit Chamber did not proceed immediately with the requested review and asked what the Chamber disagreed with in Parliament’s request. He also expressed concern about earlier correspondence that, in his view, redirected Parliament toward other tools such as requesting information from ministers or pursuing other forms of inquiry. Doran stated that such alternatives do not replace the role of the Audit Chamber when Parliament requests an independent review concerning public spending and administrative procedures.

A central point in Doran’s questioning was the language used in earlier exchanges referring to deliberations about an audit into public subsidies. He stated that Parliament required clarity on whether the Soul Beach process, specifically, would be audited. Doran therefore requested a direct response, asking whether the Soul Beach process will be audited, yes or no.

In response, the Audit Chamber referenced concerns it had previously raised about practical and legal feasibility within its mandate, including challenges related to the separation of public and private funds. The Chamber also indicated that it considered the follow-up communications received and that the subject would be taken into account in its 2026 planning.

During later portions of the meeting, the Chamber also referenced its ability to amend its annual plan as issues arise during the year, and stated that developments such as the Soul Beach matter are considered when determining audit topics. In closing remarks, Doran stated that the meeting provided the clarity he had sought on the record.

Irion: focus on impact, follow-up, transparency, and institutional credibility

MP Irion’s questions and remarks addressed the broader question of how the Audit Chamber demonstrates relevance and impact beyond publishing reports. He acknowledged the Chamber’s efforts to modernize its outreach and communications, but argued that annual reporting risks reading as self-praise if it emphasizes visibility and innovation without clearly demonstrating whether recommendations have been implemented and what measurable improvements resulted.

Irion stated that while the Audit Chamber does not have enforcement powers in the same way other institutions might, it holds moral authority, and that authority depends on credibility, restraint, and the ability to show follow-up. He urged the Chamber to present clearer information on what happens after reports are issued, including progress made by audited entities and whether recurring findings are improving or persisting over time.

He also questioned transparency practices, including the use of closed-door meetings involving the Audit Chamber. Irion stated that matters involving public spending and accountability should generally be discussed in public, except where confidentiality is necessary and clearly justified. He indicated a preference for such engagements to be open as a standard practice.

Irion further raised the issue of staff neutrality and perception of independence, asking whether the Chamber has policies to prevent staff conduct or public commentary that could be interpreted as political advocacy, emphasizing that perceived independence is central to maintaining trust.

In addition, Irion addressed the Chamber’s “Audit Intelligence” initiative, cautioning that AI tools can produce incorrect outputs and stressing the need for safeguards and human oversight. He also raised questions about how audit topics and mini-audits are selected, and whether topic selection is sufficiently tied to the issues with the greatest impact on public administration and public trust.

The Audit Chamber responded that it agrees follow-up is critical and stated it is introducing a structured follow-up mechanism, referred to during the meeting as a “progress meter,” intended to provide Parliament with periodic updates on implementation progress after reports are issued. The Chamber also stated it supports a structured requirement for ministries to submit formal action plans after major findings, including timelines and responsible officials, to improve accountability and measurability.

On meeting openness, the Chamber stated it has no objection to open meetings and noted that decisions on closed sessions rest with Parliament, with confidentiality recommended only where appropriate.

On staff neutrality, the Chamber stated it has an internal policy requiring political neutrality and indicated that breaches are addressed through internal procedures.

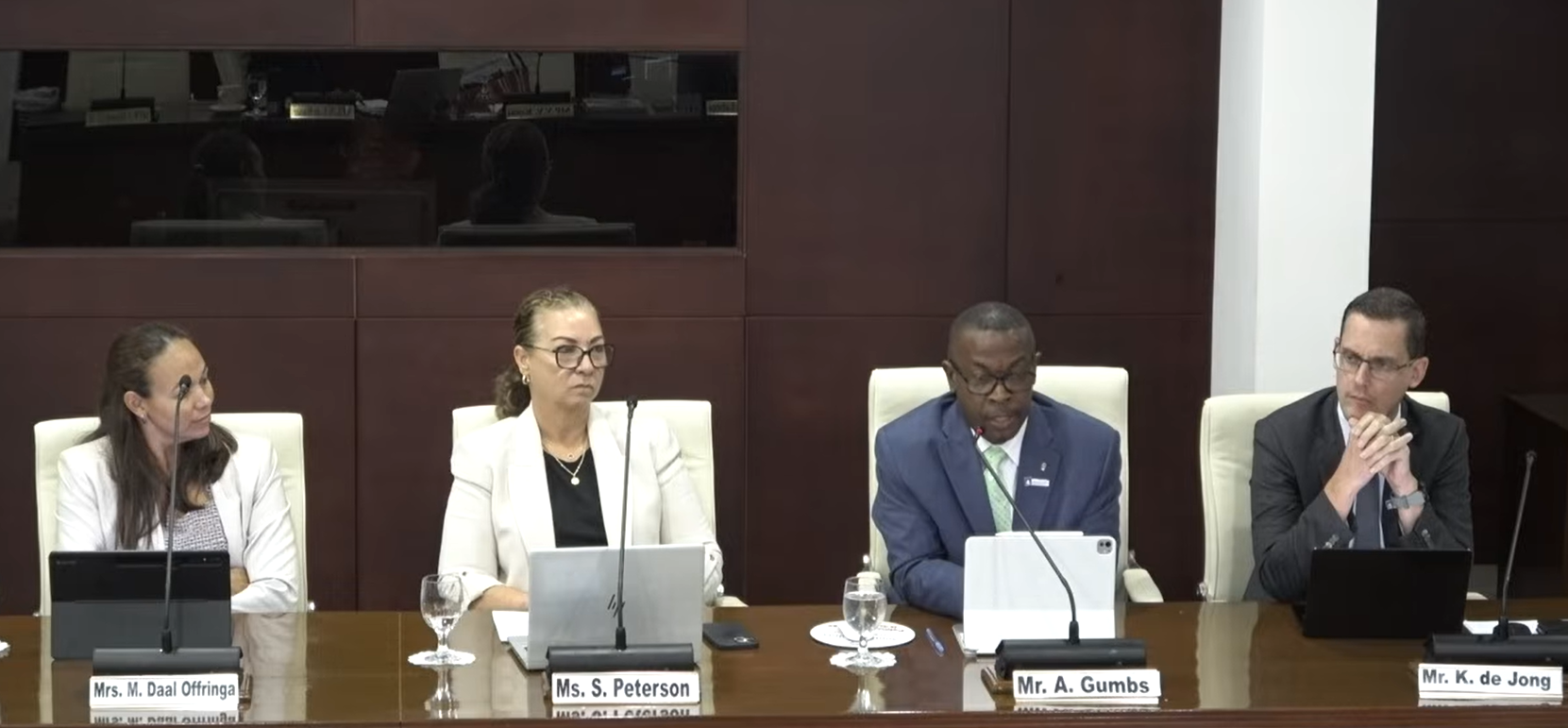

Audit Chamber presentation: mandate, independence, and Annual Report 2024

The Audit Chamber, lead by its Chairman Alphonse Gumbs, appeared to present and discuss its Annual Report 2024, published in March 2025, and to respond to questions from MPs on implementation monitoring, the timeliness of government financial statements, legal compliance in budget execution, audit planning, and transparency practices.

In opening remarks, the Audit Chamber described itself as an independent High Council of State established in the Constitution, with a mandate to provide independent, objective assurance on the management of public finances. The Chamber stated it conducts audits in line with international standards and operates independently from both government and Parliament, emphasizing that this independence is critical to effective external oversight.

The Secretary General of the Audit Chamber Keith de Jong summarized the Chamber’s legal framework and core tasks, describing three audit types: compliance audits, performance audits, and integrity-related audits, while noting that with the establishment of the Integrity Chamber, the Audit Chamber considers its resources more effectively focused on compliance and performance work.

The Chamber reported that during 2024 it completed six reports and issued several advices, covering a range of topics including the government’s 2022 financial statements, road tax allocation, government office rentals, and a mini-audit on the government’s Christmas voucher program. The Chamber also discussed staffing and budget realization and highlighted outreach initiatives designed to improve public understanding of public financial management.

The Chamber also presented an overview of an interactive learning environment and referenced the recent release of an “Audit Intelligence” assistant intended to help users find and understand information from official institutions and reports. MPs later raised questions about accuracy risks and safeguards in the use of AI tools.

The Chamber stated it anticipates finalizing its 2025 annual report by the end of February 2026 and providing it to Parliament shortly thereafter.

Other MPs: implementation monitoring, financial reporting timelines, and compliance findings

Several other MPs raised questions about how audit recommendations are implemented and tracked, and what mechanisms Parliament can use to ensure findings translate into measurable corrective action.

Questions were raised about whether ministries should be required to submit corrective action plans following major audit findings, and whether the Audit Chamber tracks implementation rates of its recommendations. MPs also asked about the status and timeliness of government financial statements, including which year would be under audit under an ideal reporting cycle, and whether the Chamber is seeing improvements in the financial management practices described by the Ministry of Finance.

The Chamber stated that the most recent audited government financial statements referenced during the meeting were for 2022. The Chamber also explained that later audits depend on the internal auditor’s completion of its review, after which the Audit Chamber is required by law to provide its report within a specified timeframe.

The Chamber also referenced recurring compliance concerns raised in prior work, including issues related to road tax allocation and the legal requirement to follow existing ordinances. MPs indicated they would use the findings in continued oversight discussions, including during budget deliberations.

Audit planning and annual themes

In response to questions on how audit topics are selected, the Audit Chamber described a planning approach that uses annual themes to guide topic selection, supported by preliminary investigations and signals emerging from earlier audits and developments during the year. The Chamber stated that its annual plan is not fully public but that themes may be shared, and that it retains the ability to amend topics within the plan when circumstances arise that warrant attention.

During the meeting, the Chamber stated that the 2026 theme is “leave no one behind,” and explained that the theme is intended to guide which areas will be reviewed, while allowing flexibility to incorporate developments that emerge during the year.

The Audit Chamber thanked Parliament for the invitation and stated that parliamentary engagement strengthens the relevance and impact of independent audit work. The Chamber reiterated the importance of implementation and follow-through, noting that transparency requires honesty and accountability requires sustained action after findings are issued.

Join Our Community Today

Subscribe to our mailing list to be the first to receive

breaking news, updates, and more.